The branchless banking network is based on banking agents. The banking agents are generally shops and postal outlets. The quality of service, cash management, and customer care will all be dependent upon the agents and the bank.

Making banking transactions is an easy task which does not require any special device. All one needs is a regular cell phone which is able to receive and send texts. Consumers can easily make transactions through their phones and can use the various mobile services provided by the financial institutions.

All mobile banking services are perfectly secure. The financial institutions have protected networks, where the transactions are kept safe and are handled meticulously. However, all consumers are required to take care of their passwords at all times, just as they would with their banking accounts.

Benefits of Mobile Banking

Mobile banking has many advantages. Some benefits of mobile banking include:

- Easy to use

- SMS is a common messaging tool amongst clients

- Relatively affordable for its consumers

- Allows the clients to get real-time information about their accounts and transactions

24 hour service - Physical visit to the bank is not required

- Mobile banking is especially beneficial to the rural populace since it provides them with the

- Ease of banking without traveling to branches and it also provides services at a lesser rate.

Mobile Banking Services

Types of transactions vary from one service provider to the other. These transactions can involve anything from:

- Text alerts

- Checking your account balance

- Bills payment

- Transfer of money

- Buy prepaid mobile vouchers

- Make donations

For details on JS bank’s branchless banking facility please follow link: https://jsbl.com/jcash/

The variety of services provided by retailers include:

-

- Maintaining an Account

- Making Mobile Phone Payments

- Purchasing Mobile Voucher

- Payment of Utility bills

- Money Transfer

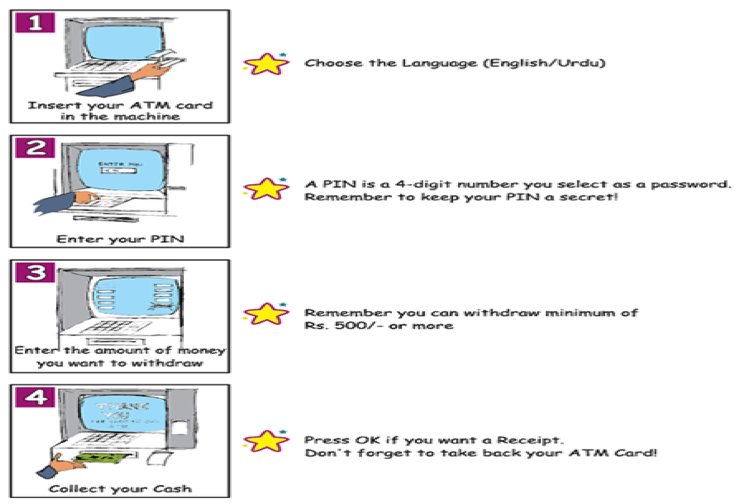

- Using an ATM

- Insert your ATM Card

- Enter your PIN

- Select ―Withdrawal

- Several Amounts will be displayed on the screen or enter the amount you want by pressing the numbered buttons

- Choose the account you want to withdraw from if asked

- Take your cash

- Take your card

- Take your withdrawal slip

To use your ATM or debit card, you must have a PIN. This is chosen when you receive your ATM or debit card. Usually a PIN is a 4- to 6-digit number that you choose and keep private. Each time you use your ATM card, you enter the same PIN.

The PIN is additional protection against someone else using your card to take money from your account. What if someone steals your wallet and finds your ATM card? What if you lose your ATM card? Only someone who knows your PIN can use your ATM card.

You must remember the number itself! Choose a number that will be easy to remember. Keep your PIN number to yourself. Don‘t tell anyone else what it is!

In addition to using it at ATMs, you can use a debit card to pay for goods you purchase in many stores. You must have the money in your account at the time of purchase. The amount of your purchase is deducted from your account immediately. You will receive a regular statement from the bank, showing the total amount deducted from your account and your remaining balance.

ATM (or bank) and debit cards are often the same card but they function in different ways. You use bank cards to withdraw, deposit or transfer cash from one account to another. For withdrawals and deposits, you choose which account you want to use. In contrast, debit cards only take funds from your bank account; usually you do not have a choice. Debit cards can be used to purchase goods. At the time of purchase, you can also choose to use your debit card to withdraw cash from your account as well as pay for the purchase. The store owner needs to have a special machine that enables such transactions with your bank.

Another type of card commonly known as a credit card; ATM and debit cards are NOT credit cards; however, they make banking much more convenient by enabling you to use your account in multiple locations at any time. But, if you use these cards to withdraw cash or buy something, you must have money in your account to cover the amount of the transaction. A credit card is different. It offers instant credit to qualified card holders.